- Marketing Accountability Standards Board (MASB)

-

Marketing Accountability Standards Board Founded 2007 Motto . . . where marketing and finance align on measurement for reporting, forecasting and improving financial returns from buyers in markets . . . short-term and over time. Website www.themasb.org The Marketing Accountability Foundation[1] and its Marketing Accountability Standards Board (MASB) is the independent, private sector, self-governing body of academics and practitioners authorized by its membership constituency to establish marketing measurement and accountability standards across industry and domain, for continuous improvement in financial performance and for the guidance and education of business decision makers and users of performance and financial information.[2]

Contents

History

Establishment of MASB was recommended by The Boardroom Project (2004–2007)[3] in response to growing demand for marketing accountability. A group of practitioners and academics saw an opportunity to increase the contribution of the marketing function, through the development of standard metrics and processes that link marketing activities more objectively and more closely to the financial performance of the firm.[4]

Over a three-year period, The Boardroom Project conducted a comprehensive review of current practices, needs and accountability initiatives underway, reaching the following conclusions:

- Marketing has been relegated to the “default” category (control costs) because it lacks metrics that reliably tie activities and costs to financial return

- While issues surrounding metrics and accountability are not being ignored, practices and initiatives underway are narrow in focus, lacking integration and generally not tied to financial return in predictable ways

- Measurement standards are essential for the efficient and effective functioning of a marketing-driven business because decisions about allocation of resources and assessment of results rely heavily on credible, valid, transparent and understandable information

- Standards across industry and domain as well as a transparent process by which to develop and select the metrics will be necessary to emerge from the current situation

- As was true for manufacturing & product quality with ISO & ANSI and for accounting & financial reporting with FASB & IASB, there is need for an industry-level “authority” to establish the standards and to ensure relevancy over time.[5]

- The development of generally accepted and common standards for measurement and measurement processes will significantly enhance the credibility of the marketing discipline, improve the effectiveness & efficiency of marketing activities, guide continuous improvement over time, and enable Marketing to move from discretionary business expense to board-level strategic investment

MASB Mission

The Mission of MASB is to “Establish marketing measurement and accountability standards across industry and domain for continuous improvement in financial performance and for the guidance and education of business decision makers and users of performance and financial information.” [2]

Role of MASB

MASB sets the standards and processes necessary for evaluating marketing measurement in a manner that ensures credibility, validity, transparency and understanding.

MASB does not endorse specific measures. Rather, it documents, reveals and highlights how various measures stack up against the Marketing Metric Audit Protocol (MMAP). The belief and assumption is that the market will select specific measures based on these evaluations. MASB’s Dynamic Marketing Metrics Catalogue will be the primary vehicle for documentation and publication.

MASB also exemplifies how to evaluate and identify ideal measures according to MMAP for specific marketing activities such as TV and On-Line advertising and/or any other activity or area for which there is need as identified by its membership constituency.

MASB delves into practices underlying the development and management of ideal measures as well as those practices utilized to create knowledge, determine causality, and apply to process management for improved return.

Overall, MASB serves at the industry level in this fashion and works with “open due process”.[2]

Precepts of Conduct

MASB Directors operate according to the following precepts of conduct:

- Be open and objective in decision making

- Weigh carefully the needs and views of constituency

- Promulgate standards when:

- Logical flow of the argument is tight

- Empirical support material is convincing

- Conclusions are managerially meaningful

- Scientific evidence pros and cons are acknowledged

- Benefits exceed costs

- Ensure transparency of the standards setting activity through open due process

- Bring about needed change while minimizing disruption

- Review effects of past decisions (interpret, amend, replace) [6]

MASB Projects

Work of the MASB is conducted on a Project basis and organized into three overall categories: Standards, Research and Concepts.

Prioritization is based on the following considerations:

- Pervasiveness of the Issue

- Alternative Solutions

- Technical Feasibility

- Practical Consequences

- Convergence Possibilities

- Cooperative Opportunities

- Resources

Projects on the MASB Agenda were recommended by MASB Charter Members, influenced in part by feedback from C Level interviews. They have been prioritized according to MASB resources:[7]

Projects Completed

- Marketing Productivity, Effectiveness and Accountability [8]

- Objectives of Marketing Standards [9]

- The Role of Standards: Academic Review [10]

- C Level Views on Marketing Accountability [11]

Projects Ready for Industry Feedback

- Marketing Metrics Audit Protocol [12]

- Measuring TV According to MMAP – An Example [13]

- Practices Underlying an Ideal Metric [14]

Projects Underway

- Measuring & Improving the Long-Term Impact

- Common Language for Marketing Activities & Metrics on Wikipedia

- Marketing Metrics Profiled to MMAP

- Measuring & Improving Return from Interactive

- Measuring & Improving CPG Return With CLV

- FASB/MASB Partnership for Aligning GAAP/MMAP[5]

- Brand Investment Model and Discipline [15]

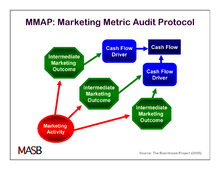

Marketing Metric Audit Protocol (MMAP)

The Marketing Metric Audit Protocol (MMAP) is a formal process for connecting marketing activities to the financial performance of the firm.[5]

The process includes the conceptual linking of marketing activities to intermediate marketing outcome metrics to cash flow drivers of the business, as well as the validation and causality characteristics of an ideal metric. Cash flow both short-term and over time is the ultimate metric to which all activities of a business enterprise, including marketing, should be causally linked through the validation of intermediate marketing measures.

The process of validating the intermediate outcome measures against short-term and/or long-term cash flow drivers is necessary to facilitate forecasting and improvement in return.

See Marketing Metric Audit Protocol and Measuring TV According to MMAP – An Example. [16]

MMAP Metric Profiles

MMAP Metric Profiles is a Catalogue of Marketing Metrics that provides detailed documentation regarding the psychometric properties of the measures and specific information with respect to reliability, validity, range of use, sensitivity . . . particularly in terms of validity and sensitivity with respect to financial criteria.

Most commercial providers offer little detail about their measures. Most of the publicly available information focuses on integrated suites of products and services with little technical information or reference to characteristics of specific measures that would allow profiling according to MMAP.

The Metrics Catalogue is provided on the MASB website as metric providers undergo the audit and their offerings are profiled according to MMAP.[16]

Marketing Accountability Foundation

The Marketing Accountability Foundation (MAF)[1] is the independent, private sector, self-governing organization authorized by its membership constituency to:

- Establish & improve marketing measurement & accountability standards

- Educate constituents about those standards

- Provide oversight, administration & funding for its standards-setting Board (MASB) and its Advisory Council (MASAC)

- Select Directors of the MASB and MASAC

- Protect the independence & integrity of the standards-setting process

The Foundation is incorporated exclusively for charitable, educational, scientific, & literary purposes within the meaning of Section 501(c) (3) of the Internal Revenue Code.

Sources of funding include Membership Dues, Projects, Workshops, Technical Services, Publications, and Training, Advisory & Auditing Services.

Membership

Membership is organization-based, and open to Marketers, Business Schools, Measurement (Modeling & Software) Providers, Media Providers, Media & Advertising Agencies, Industry Associations & Independent Consultants. Membership development has been targeted to fill the Foundation Trustee, MASB Director, Advisor and Project Leadership positions.

Founding and Charter Members in order of joining include: University of California Riverside, The MMAP Center, Starcom MediaVest Group, The Nielsen Company, The Advertising Research Foundation (ARF), Marketing Science Institute (MSI), UCLA Anderson School of Management, Columbia University, MarketShare Partners, ConAgra Foods, University of Michigan, American Marketing Association (AMA), Association of National Advertisers (ANA) , Kimberly-Clark, Foresight ROI, Blue Marble Enterprises, Mobile Marketing Association (MMA), The Wharton School, NYU Stern School of Business, CoreBrand, The Coca-Cola Company, Darden School of Business, University of Cologne, LogicLab. click here.[17][5]

References

- ^ a b MASB. Marketing Accountability Foundation (MAF). [cited 8 December 2010]

- ^ a b c MASB. MASB Mission. [cited 8 December 2010]

- ^ MASB. The Boardroom Project.[cited 8 December 2010]

- ^ Gregory, James. "In Search of Brand Accountability." Branding Strategy Insider. 9 July 2010. [cited 19 January 2011]

- ^ a b c d Neff, Jack. "Mass of Metrics May Mean Marketers Know Less." Advertising Age. 20 September 2010. [cited 19 January 2011]

- ^ MASB. Precepts of Conduct. [cited 8 December 2010]

- ^ MASB. MASB Projects. [cited 8 December 2010]

- ^ The Boardroom Project. Contributing to the Bottom Line: Marketing Productivity, Effectiveness, and Accountability. July 2005. [cited 8 December 2010]

- ^ The Boardroom Project. Objectives of Marketing Standards. August 2006. [cited 8 December 2010]

- ^ Stewart, David. Academic Review: The Role of Standards. February 2007. [cited 8 December 2010]

- ^ Plummer, Joe, and Blair, Meg. C-Level Views on Marketing ROI. July 2008. [cited 8 December 2010]

- ^ MASB. Marketing Metric Audit Protocol (MMAP). February 2009. [cited 8 December 2010]

- ^ MASB. Measuring and Improving the Return from TV Advertising (An Example). April 2008. [cited 8 December 2010]

- ^ MASB. Practices & Processes Underlying the Development & Management of an "Ideal Metric." October 2010. [cited 8 December 2010]

- ^ MASB. MASB Projects: Underway. [cited 8 December 2010]

- ^ a b MASB. MMAP. [cited 8 December 2010]

- ^ MASB. Charter Membership. [cited 8 December 2010]

External links

Categories:- Marketing organizations

Wikimedia Foundation. 2010.